Crossing The Chasm | Part II

A continued summary of "one of the most transformative books in technology entrepreneurship".

This is Part II of a two-part series. Part I can be found here:

Crossing the chasm and entering the mainstream market is a considerable challenge. It's an act of courage, bravery, and aggression. As Moore says, "No one wants your presence. You are an invader."

Moore uses the Allied invasion of Normandy on D Day to guide the reader's thinking. Crank the Saving Private Ryan soundtrack and get to reading (emphasis mine):

"Our long-term goal is to enter and take control of a mainstream market (Eisenhower's Europe) that is currently dominated by an entrenched competitor (the Axis). We must assemble an invasion force comprising of other products and companies (the Allies). Our immediate goal is to transition from an early market base (England) to a strategic target market segment in the mainstream (beaches at Normandy). Separating us from our goal is the chasm (the English Channel). We are going to cross that chasm as fast as we can with an invasion force focused directly and exclusively on the point of attack (D Day). We'll force the competition out of our targeted niche markets (secure the beachhead), then move out to take over the additional market segments (districts of France), on our way to overall market domination (the liberation of Europe)."

The beauty of the "D Day" strategy is that everyone has a set goal:

Take Normandy. As Moore says, "if we don't take Normandy, we don't have to worry about how we're going to take Paris." By focusing on such a small space (Normandy beaches), the attackers had a higher chance of taking the beach.

Companies that successfully "take the beach" do so by hyper-focusing on the tiniest niche inside the Early Majority market. They do this by starting a fire and getting a white-hot center burning.

To start the fire, Moore says companies should "ensure that our first set of customers completely satisfy their buying objectives."

To completely satisfy our customers we need one thing: a whole product. Moore describes a whole product as "the complete set of products and services needed to achieve the desired result."

Creating The White-Hot Center

Think of the whole product as a white-glove service offered to the highest-priority customer set. Yes, it's expensive. Yes, it doesn't scale. But that's the point. You do what you have to do to get that first set of references in the Early Majority market.

Bill Gurley, in his first episode on Invest Like The Best, discussed this idea of unscalability and white-hot center (emphasis mine):

"I have found the majority of, one of my rules for getting a marketplace off the ground, or you could say for UGC players, do tons of unscalable things. And if you took 90% of the entrepreneurs that have been to business school and understand scaling, it drives them nuts. Like they don't understand. They'll say, "Oh, we can't do this. How we'll ever do that at scale?" And I'm like, "We're not going to do it at scale. This is a flywheel. We're trying to get the flywheel spinning.""

Gurley uses two examples of early-stage companies doing unscalable things to create the white-hot center:

Glassdoor:

"I'll give you an example in the Glassdoor case. I think the very first company that was reviewed was Cisco and the founders went to the Starbucks near Cisco with a pad of paper and interviewed people for reviews, right? There's zero chance that's going to be the long-term business effort against that, but you got to see the market."

Yelp:

"Jeremy would go to nightclubs with t-shirts to get the Yelpers excited about what they were doing. And there's no way he's going to go to every business on the Yelp platform, you're trying to get the thing to come alive where there's passionate participants that care about the quality of the reviews. Jeremy focused on nightclubs in San Francisco, got the fire burning really, really bright and then had it bleed with quality."

Gurley's two examples are a perfect reminder of Moore's above quote, "If we don't take Normandy, we don't have to worry about how we're going to take Paris." Glassdoor needed to capture Cisco and Starbucks with a pad of paper and in-person interviews.

If they didn't win with that, there was no point in trying to scale (i.e., "take Paris"). Similarly, if Yelp couldn't excite San Francisco Nightclubs to leave reviews on their site, they shouldn't expand their product because they haven't even secured the beach.

One weapon early-stage companies can use to take the beaches and advance towards Paris is word of mouth. Word of mouth is the kindling that helped Glassdoor and Yelp get their fire burning brighter than the competition, even when the challenger had more venture-dollar ammunition at their disposal. Moore identified word of mouth reputation as a key to breaking into a new market (emphasis mine):

"Numerous studies have shown that in the high-tech buying process, word of mouth is the number one source of information buyers reference, both at the beginning of the sales cycle, to establish their 'long lists,' and at the end, when they are paring down their short ones. Now, for word of mouth to develop in any particular marketplace, there must be a critical mass of informed individuals who meet from time to time and, in exchanging views, reinforce the product's or the company's positioning."

Critical mass and white-hot center. Two names to describe the same phenomenon of capturing that early batch of customers within your next addressable market.

Example of Storming The Beach: Documentum

Documentum, a document management software application, is one company that successfully crossed the chasm. Jeff Miller became CEO of Documentum in 1993. During the three years before Miller took control, the company failed to grow revenues past ~$2M/year.

One year after assuming the CEO position, Miller led Documentum to $8M in sales. They then did $25M the following year and $45M the year after that. By applying Moore's original edition of the book, Miller took Documentum from a meandering $2M sales company to $75M and a listing on the NASDAQ.

But what precisely did Miller do that made the company change so dramatically? Let's follow the Chasm blueprint to see how he did it.

Step 1: Select A Beachhead Market Segment

Miller did this by surveying Documentum's client experience to find a hyper-niche service market: regulatory affairs departments in Fortune 500 pharmaceutical companies. In effect, Miller segregated Documentum's market to roughly forty companies globally.

Purposely shrinking your market goes against every conventional business strategy textbook. Conventional wisdom says to target the most significant market possible. The whole "shoot for the moon, and you might catch the stars" mantra. Documentum went the complete opposite route. They took their original addressable market ("all personnel who touch complex documents in all large enterprises") to, as Moore notes, "maybe one thousand people total on the planet?"

Step 2: Solve A Crucial Pain Point

Shifting the company's focus to a thousand people, Miller identified the highest pain-point for his new-found customer base: the patent approval process. Moore describes the paint point (emphasis mine):

"The patents have a 17-year life, and a successful patented drug generates on average about $400M per year. Once the drug goes off-patent, however, its economic returns plummet. Every day spent in the application process is a day of patent-life wasted. Pharmaceutical companies were taking up to one year to get their first application filed -- not a year to get it approved, a year to get it submitted!"

Patent approval applications range between 250-500 thousand words. That's not a typo. Inside the hundreds of thousands of pages include clinical trial study data, correspondence between researchers, manufacturing databases, and research lab notebooks.

Every patent approval needed these items. And it was a nightmare for drug companies because that's not what they wanted to do. A drug company should focus its efforts on finding and developing the best drugs, not creating the most optimal patent approval application.

Documentum solved this problem and gained the trust of 30 out of the top 40 companies in their niche.

Step 3: Create A "Bowling-Pin" Marketing Effect

Documentum eventually generated over $100M in revenues. They didn't achieve that by staying inside the regulatory approval process. Instead, they used the "Bowling-Pin" niche marketing effect.

Bowling-Pin marketing is a fancy way of saying Documentum's initial customers found ways to use the company's software in other areas of their business. Moore provides an excellent example of the "Bowling Pin" at work (emphasis mine):

"Once [the software] got to the floor, the plant construction and maintenance contractors, who were using it to assemble and maintain documentation on all the systems and procedures in the factory, recognized that factories in related process industries had the same needs, and they took the product into regulated chemicals, non-regulated chemicals, and oil-refineries... When the product hit the refineries [...], the IT people recognized a tool that could solve a major problem in their upstream business, exploration and production ... And then that success caught the attention of Wall Street, who saw that the same facilities would help them get better control over their swaps and derivatives business."

It's niche marketing all the way down. Once you learn the effect, you begin to see "Bowling-Pin" marketing all around you.

Square, for example, solved a hyper-niche problem for one person (Jim McKelvey) who couldn't accept a credit card as payment for his glass faucets. Now, Square generates $9B+ in revenue, employs 4K people, and has a beautifully elegant Cash App business.

Square is arguably one of the clearest examples of "Bowling-Pin" marketing in history, but it's far from the only one. Facebook (FB) is another disciple of this strategy. Zuckerberg created "The Facebook" exclusively for Harvard students. Then he expanded into all Ivy League schools. The rest, of course, is history.

Whether it’s Documentum, Square, or Facebook, each company had one thing in common: they got the initial fire burning brightly by hyper-focusing on the smallest possible niche.

Moore reveals two keys to the entire Bowling-Pin marketing sequence (emphasis mine):

Key #1: "The first is knocking over the head pin, taking the beachhead, crossing the chasm. The size of the first pin is not the issue, but the economic value of the problem it fixes is. The more serious the problem, the faster the target niche will pull you out of the chasm."

Let's stop here before going to the second key by examining Square's strategy to Moore's explanation. Note how Moore says, "the size of the first pin is not the issue." That's important because it means a company can focus on solving the biggest problem, not the highest-dollar-value proposition.

Square could afford to tackle one person's most enormous problem because if it solves it for one, it can solve it for many (as long as there are more people with the same problem). Done correctly, providing a solution creates self-reinforcing scaled word-of-mouth benefits.

That first customer (or batch of customers) will tell others (likely those experiencing the same problem) of their solution. That's what Bill Gurley means when he says he wants to see a product/service "bleed" before "throwing venture dollars" at it. If you can solve that initial customer paint point (trigger the bleed), you can scale it with ease because others have the same problem.

Key #2: "The second key is to have lined up other market segments into which you can leverage your initial niche solution. This allows you to reinterpret the financial gain in crossing the chasm. It is not about the money you make from the first niche: It is the sum of that money plus the gains from all subsequent niches."

In other words, a company should always have a broader vision for its product or service apart from its initial pain-point customers. The first batch of customers isn't the final market. It’s the beachhead we need to capture to cross the chasm.

Once a company crosses the chasm, it needs a more extensive market to continue solving customer problems. Translated to investing jargon, companies need both a hyper-targeted niche and a large TAM (total addressable market). The duality of focus is what makes the Bowling Pin strategy effective.

It allows a company to identify the largest pain-point for the smallest cohort of customers while simultaneously keeping the larger market in view.

There is a bit of a catch-22 with the second key, as Moore points out (emphasis mine):

"If the executive council cannot see the extended market, if they only see the first niche, they won't fund. Conversely, if you go the other way, and show them only an aggregated mass market, the end result of the market going horizontal and into hypergrowth, they will fund, but then they will fire you as you fail to generate these spectacular numbers quickly."

Paypal is an excellent example of focusing on a larger audience while solving a hyper-specific problem. The company's first product helped eBay sellers accept payment for the goods offered on the site. Paypal sparked the initial burn (or bleed) by depositing $10 into new Paypal users' digital wallets. Thiel, Musk, and company did things that didn't scale (i.e., give people free money) to capture the white-hot center, to take the beachhead.

From there, the company expanded into international eBay accounts to service a wider-range of customers. Finally, Paypal leveraged its target niche to develop its off-eBay business. The move kickstarted what we now know as "today's Paypal."

Next, we'll focus on the strategic differences in crossing the chasm for application-based vs. platform-based businesses.

Applications vs. Platforms

Moore says there are different risk/reward trade-offs in chasm-crossing strategies depending on whether you market a platform or an application product. Applications, by default, find it easier to cross the chasm than platforms. Moore explains (emphasis mine):

"For the actual chasm crossing[,] applications have a huge advantage. That is because disruptive innovations are more likely to be championed by end-users than by the technology professionals that operate the current infrastructure."

Users/Customers see applications in real-time. They can see when one fixes a problem and when one doesn't. This first-rate problem-to-solution connection allows applications to generate a faster word-of-mouth reputation amongst ordinary users.

Platforms are different. You can't see platforms solving problems the way you can with apps. That makes crossing the chasm with a platform product more difficult. The other obstacle facing platform chasm-crossing is their target customer base.

While applications target specific end-users (think Square's glass-blower customer), platforms target domain experts like IT divisions inside more prominent companies. Moore unravels why this causes issues for platforms attempting to cross the chasm (emphasis mine):

"Platforms, by contrast, are multi-purpose by definition. They are infrastructure and as such are the domain of the IT community. Charged with maintaining the security, reliability, and performance of the current infrastructure, this group is not quick to adopt disruptive technologies which require widespread reengineering of systems."

In other words, incumbents love platform models because of their high switching costs. That's great if you're already on the beach. But for those companies trying to secure a beachhead and cross the chasm, they need a way to cloak their platform. The secret, Moore suggests, is disguising a platform as an application (emphasis mine):

"To accelerate the adoption of platforms, then, vendors must clothe them in applications clothing. That is, they must tie them directly to an application in order to gain the end-user sponsorship necessary to secure a beachhead."

What Moore is suggesting, to my understanding, is that platforms should create applications for specific use cases that lead back to the original platform center. For example, accounting software solves myriad particular problems for an accountant's tasks, yet each application leads back to the central platform.

Focus on Target Customers, Not Target Market (There's A Difference!)

Early-stage products should focus on target customers, not a target market. Here's the difference. A target customer is a hyper-niche user that experiences a tremendous pain point your product is trying to solve. A target market is "small and medium-sized business accounting software." As Moore warns, choosing to focus on a target market instead of a target customer could lead to chasm crossing failure (emphasis mine):

"The place most crossing-the-chasm marketing segmentation efforts get into trouble is at the beginning, when they focus on a target market or target segment instead of on a target customer."

This warning echoes the successes of the businesses we covered earlier in the essay. Companies like Paypal and Square didn't set out to conquer the entire digital banking space or dominate the point-of-sale process for small-to-medium-sized businesses. They both solved a problem for a target customer -- eBay for auction sellers and Square for glass-blowers.

Another reason why targeting customers works is that it’s easier to envision a customer, not a massive market. Companies trying to pitch their product or service are better off using examples of individuals that would benefit from their service instead of saying, "all we need to do is capture 1% of this gigantic market!"

By individualizing the problem and the target users, potential customers/investors can visualize themselves using the product or service. You can't get that with broad market-specific data, as Moore reminds us (emphasis mine):

"As soon as the numbers get up in a chart -- or better yet, a graph -- as soon as they thus become blessed with some specious authenticity, they become the drivers in high-risk, low-data situations because these people are so anxious to have data. That's when you hear them saying things like, 'It will be a billion-dollar market in 1995. If we only get 5 percent of that market ...' When you hear that sort of stuff, exit gracefully, holding on to your wallet."

Generally, high-tech product marketers assume investors and customers want to know how big a problem their product solves. While that's true, that's not how companies should frame it. Instead, focus on the individual user's pain point. Then, and only then, can you scale that individual's pain point to some abstract addressable market.

To get from target customer to target market, you need a checklist. Luckily, Moore gives us a blueprint! Let's check it out.

Moore's Market Development Strategy Checklist

The Market Development Strategy Checklist helps companies determine the one target customer to attack to secure the beachhead into a larger market. There are two "stages" to the checklist. The first stage includes four chasm-crossing factors.

Score a low number on any one of these initial four, and you have what Moore calls a "show-stopper." No, it's not a gorgeous model. It's a sign that your product won't cross the chasm, and you should give up. Moore explains the first four factors, which are as follows:

Target Customer: "Is there a single, identifiable economic buyer for this offer, readily accessible to the sales channel we intend to use, and sufficiently well-funded to pay the price for the whole product?"

Compelling Reason To Buy: "Are the economic consequences sufficient to mandate any reasonable economic buyer to fix the problem called out in the scenario?"

Whole Product: "Can our company with the help of partners and allies field a complete solution to the target customer's compelling reason to buy in the next three months such that we can be in the market by the end of next quarter and be dominating the market within twelve months thereafter?"

Competition: "Has this problem already been addressed by another company such that they have crossed the chasm ahead of us and occupied the space we would be targeting?"

Each factor gets a rating between 1 and 4, so the highest a company can score in the first stage is 20, and the lowest they can achieve is 4. While geared towards product marketers of high-tech firms, these four factors are perfect filtering questions for public equity investors.

Imagine how much better your investments could be if you only Invested in companies that scored a 12 or higher on the first four factors!

If a company passes the first stage, they move on to the second stage. Moore calls the second stage the "nice to have" category. The five factors in the second stage are:

Partners & Allies: "Do we already have relationships begun with the other companies needed to fulfill the whole product?"

Distribution: "Do we have a sales channel in place that can call on the target customers and fulfill the whole product requirements put on distribution?

Pricing: "Is the price of the whole product consistent with the target customer's budget and with the value gained by fixing the broken process?"

Positioning: "Is the company credible as a provider of products and services to the target niche?"

Next Target Customer: "If we are successful in dominating this niche, does it have good 'bowling pin; potential? Will these customers and partners facilitate our entry into adjacent niches?"

As Moore notes, the above five factors are "nice to haves" and assume that the product in question meets the first stage’s requirements. But again, ask yourself these questions when analyzing public companies. A company might have a great product, but if their distribution sucks, what's the point?

Likewise, a high-tech product might save customers hundreds of thousands of dollars, yet the company underprices their offering, leaving precious dollars on the table. Or even worse, what if a company looks promising in securing the beachhead but has no "bleed" -- no way to break into adjacent markets?

These questions pertain mostly to early-stage companies. But they also work as channel checks for mature businesses as they continue to grow and find new growth avenues.

Market Size Matters, But Not How You'd Think

The book has a way of repeating similar yet valuable themes throughout its chapters. Market size is a great example. When a product is on the cusp of entering its target market, you should ask, "how much revenue can this market generate?"

After all, revenues matter because we'll need profits at some point. But Moore offers an unconventional view on the topic of the total market size (emphasis mine):

"At this point, people normally think that bigger [market] is better. In fact, this is almost never the case. Here's why. To become a going concern, a persistent entity in the market, you need a customer market that will commit to you as its de facto standard for enabling a critical business process. To become that de facto standard, you need to win at least half, and preferably a lot more, of the new orders in the segment over the next year."

In short, any company’s goal as it crosses the chasm is to monopolize how its target market users solve a specific problem. Take Oracle's databases, for example.

When customers needed a solution to a pain point (storing data), they used Oracle's software product. When a mom-and-pop general store wanted to accept credit cards but didn't want to pay massive merchant fees, they used Square's card reader.

All these examples highlight the power of monopolizing the solution to a target customer's most prominent pain point. Moore reminds us that "the goal is to become a big fish in a small pond."

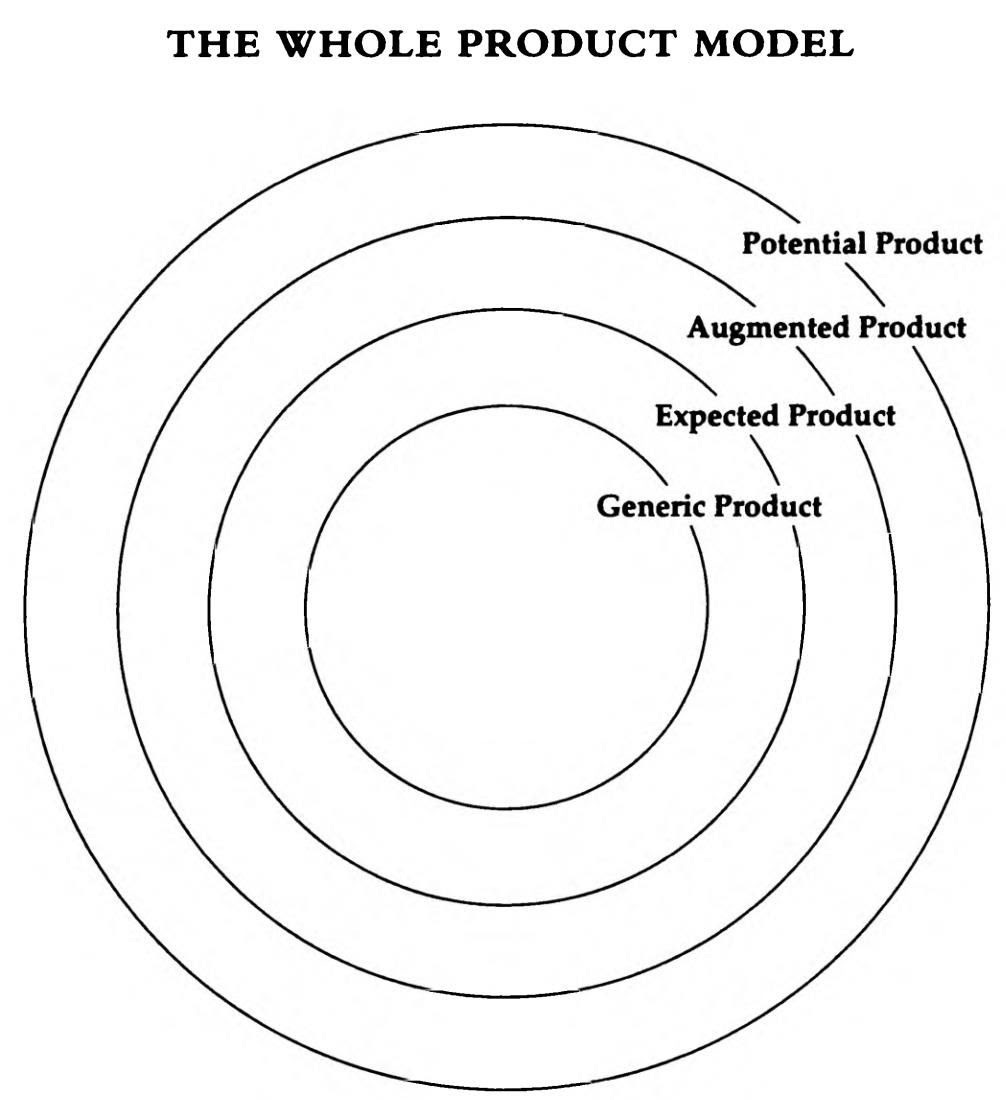

The Whole Product Model

To successfully cross the chasm and win the market, a company needs to build a whole product model. You've read that term a few times in this essay, so let's break down what it means. Moore defines the Whole Product Model as (emphasis mine):

"The concept [of the whole product model] is very straightforward: There is a gap between the marketing promise made to the customer -- the compelling value proposition -- and the ability of the shipped product to fulfill that promise. For that gap to be overcome, the product must be augmented by a variety of services and ancillary products to become the whole product."

There are four different perceptions of how a customer defines "product" (with Moore's definitions):

Generic Product: What's shipped in the box and covered by the purchase contract.

Expected Product: What the consumer thought she was buying when she bought the generic product.

Augmented Product: The product fleshed out to provide the maximum chance of achieving the buying objective.

Potential Product: The product's room for growth as more and more ancillary products come on the market and as customer-specific enhancements to the system are made.

Moore then uses the Internet Browser Category as an example of the four stages of product:

Generic Product: Set of functions first made famous by Mosaic (remember, it's the late 90s).

Expected Product: Portability to each of the popular client platforms, including Unix and Macintosh.

Augmented Product: Includes plug-ins from third parties to provide additional features.

Potential Product: Reconstruction of consumer purchasing

The cool thing about the Whole Product Model is that we can superimpose it onto our TALC model. For example, as we move from left to right on the TALC bell curve, our Whole Product Model’s outer circles become most important. The move of importance outward makes intuitive sense.

Innovator customers don't care about the Augmented or Potential Product. They want to half-baked version with all the bugs and glitches. That said, if you’re going to win the target market and cross the chasm, you need to win the pragmatists. You need to win the majority. To do that, you need the whole product. Moore explains below (emphasis mine):

"To get to the right of the chasm -- to cross into the mainstream market -- you have to first meet the demands of the pragmatist customers. These customers want the whole product to be readily available from the outset. They like a product such as Microsoft because there are not only books in every bookstore about how to use it but also seminars for training, office hot-line support, and a whole cadre of temporary office workers already trained on the product."

That phenomenon of creating the whole product is why we see inferior "generic products" dominate mainstream markets. The Bloomberg Terminal is an excellent example. The mainstream market hates that thing. The UI/UX is in a bar reminiscing about the days of Mainframe computing, it’s too expensive, and you need fingerprint access and can't share the software.

Yet everyone In finance uses it.

Why? Partly because everyone else uses it. But there is also an argument that Bloomberg has the best Whole Product. My college taught Bloomberg to its finance students as a credited class. There are YouTube courses dedicated to teaching the Bloomberg terminal. Heck, the software even has its special keyboard (augmented product).

Moore understood this phenomenon well and remarked, "In every case, there are strong arguments that they [customers] are preferring an inferior product -- if you look only at the generic product. But in every case, they are preferring the superior product, if you look at the whole product."

Creating Competition: An Unconventional Way To Win Customers

Here's an exciting idea. If a new product wants to win a target market, it should help customers identify other competition to solve the problem. I know. Who wants to create competition? Didn't the philosopher Peter Thiel preach the benefits of monopoly? Here's why it makes sense (to the book):

"Pragmatist buyers do not like to buy until there is both established competition and an established leader, for that is a signal that the market has matured sufficiently to support a reasonable whole product infrastructure around an identified centerpiece."

Pragmatists love comparing things, so give them something (or someone) to judge your product’s worth. The steps are simple. First, locate your product within a buying category that has established credibility and market maturity.

Then, select comparable products to act as fair competition. Finally, position your product as the indisputably correct buying choice. Let's look at an example from Intuit's Quicken to see how they created the competition to win their target market.

Quicken helps individuals manage their finances. Today, Intuit's products are market leaders and household names. But it wasn't always like that. Let's pick it up in the book (emphasis mine):

"When Quicken was first introduced into the market, the best-selling program was Andrew Tobias's 'Managing Your Money.' From a product-centric point of view, it was far richer in functionality than Quicken, offering portfolio analysis and other financial modeling capabilities. To the 'financial enthusiasts' who made up the early market for these products, it as clearly the preferred choice, and Intuit was doomed if it continued to play the game on that turf."

The above paragraph paints a grim picture of the future of Intuit's Quicken product. The company had to differentiate itself from its peers to capture the beachhead. So they found a simple value proposition: "make it easier to pay bills."

Elegant, but there was no established mainstream category for that service. The company realized most of its target customers used paper checks and balanced their checkbooks manually. Intuit penetrated this market, creating its own patented check-reader solution, and in turn, a whole product solution. Now we have Quicken's updated value proposition after Introducing the competition (emphasis mine):

"The market alternative is paper and pen checking. That is the familiar alternative. What we are going to offer is more speed and convenience during bill paying plus the opportunity to control one's finances by seeing where the money goes plus a more more organized set of resources with which to tackle tax time."

In what looks like a stroke of genius, Quicken turned their original competitor Managing Your Money, into a "reference beacon" for customers to switch to Quicken! Moore explains this concept:

"Intuit could now use [Managing Your Money] as a reference beacon. That product, they could say, is the one for financial enthusiasts who want to analyze their investment portfolios. This product is for ordinary householders paying their monthly bills."

Intuit's genius boils down to the power of Positioning. Moore mentions four Positioning Principles every product should follow:

Positioning, first and foremost, is a noun, not a verb: This means positioning is an attribute associated with a company, not something the company does

Positioning is the single largest influence on the buying decision: Buyers' shorthand for evaluating potential purchases

Positioning exists in people's heads, not in your words: Put yourself in the shoes of your customers, then say what they believe will likely live in their world

People are highly conservative about entertaining changes in positioning: People have a hard time changing their preconceived beliefs about the world, so don't make them change.

Conclusion: Storm The Beach, Secure The Beachhead, Win The Market

Crossing The Chasm is easily one of my favorite books on technology, product development, and marketing. Geoffrey Moore does an excellent job synthesizing complex ideas into bite-sized chapters while providing real-world examples of his work theories.

If you learned anything from this book review, I hope you understood the following:

There are five types of customers:

Innovators, Early Adopters, Early Majority, Late Majority, and Laggards

Winning the approval of the first two customers gives you a shot at crossing the chasm into the majority. To cross the chasm, you need to target a specific niche within the mainstream market (i.e., get the fire burning)The best way to get the fire burning is to do things that will not scale with your earliest customers

There are three steps to securing the beachhead: Select a Beachhead Market Segment, Solve a Crucial Pain Point, Create a Bowling Pin Marketing Strategy

There are two keys to a great Bowling Pin Marketing

Strategy #1: Take out the headpin

Strategy #2: Line up other market segments to penetrate. It's easier to cross the chasm as an application product vs. a platform. Focus on the smallest niche customers possible. Don't worry about a large addressable market. If your product works, the scale will follow. There are four types of products that you sell: Generic, Expected, Augmented, and Potential. Create competition within your product market so that the majority base can compare you against the others and hopefully see your product as superior.