AutoStore Holdings (AUTO)

40%+ Revenue Growth + 50% EBITDA Margins + Massive TAM = One Incredible Business

AUTO is the world’s leading cubic storage automation company with nearly 30 years of experience and over 667 installations to date.

The company helps customers turn bulky, antiquated fulfillment centers into fast-moving, highly efficient autonomous machines. To do this, AUTO combines three basic components:

Bins

Grids

Ports

AUTO vertically stacks its 2x1x1 bins, saving companies hundreds of square feet in warehouse space (which reduces rent costs). On top of these bins is a two-dimensional aluminum grid. The grid enables AUTO’s robots to move in any direction to retrieve any container.

My first question was, “That’s cool. But how do they get the bins at the bottom?” The answer is genius.

AUTO’s robots automatically determine which items in each bin are “hot” (i.e., best sellers). These best-sellers stay near the top so the robots can quickly access those items.

Other, less popular items get sent to the bottom of the stack. From here, an AUTO bot can extract each higher bin until they retrieve their desired box. Then, other robots can help displace the containers the previous robot needed to move.

Words don’t do it justice. Just watch this video.

Anyways, once the robot finds the correct bin, it transports it to the port, where a warehouse worker can seamlessly collect and ship the item while documenting inventory.

AUTO: Sticky Business w/ Massive Scale Advantage

AUTO is a highly sticky cog in any company’s order fulfillment system. So much so that the company has never lost a customer since its founding. Let’s shift to AUTO’s massive scale advantage against its competition.

The company boasts over 500 customers with 667 warehouse installations and 22,000 robots. To put that in perspective, AUTO’s next closest competitors (Ocado and Attabotics) sport a combined 15 installations.

There are three main benefits to AUTO’s massive scale. First are operational benefits. Given its size, AUTO can support more customers than its competition. The company offers up to 650 picks per hour (robot picks), over 1 million SKU capacity, and 90% space utilization.

Then there are the data benefits. Since AUTO has more robots and installations than competitors, it can gather more data than other companies. This data leads to better performance and less downtime. For example, AUTO’s robots sport a 99.9% picking accuracy and 99.7% uptime.

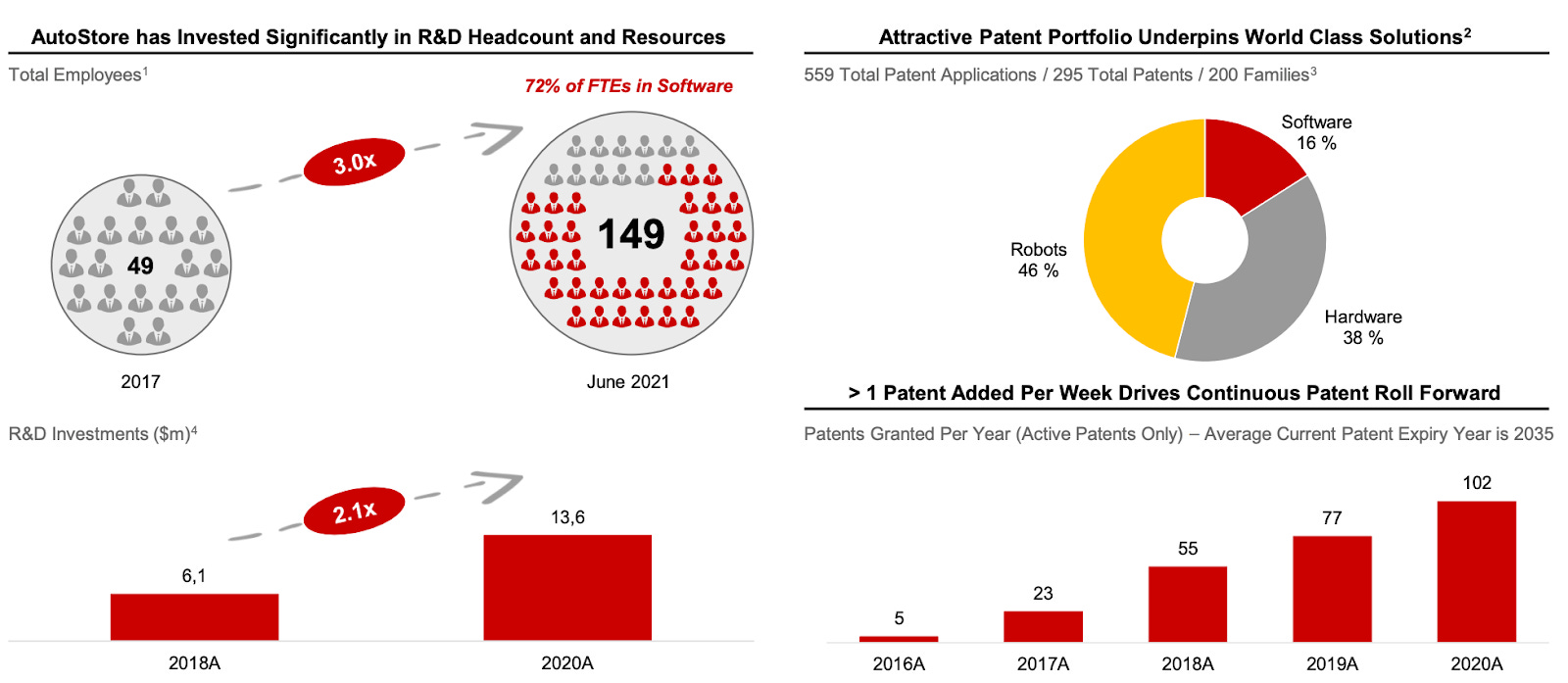

Finally, AUTO’s scale allows them to hire more engineers to further invest in R&D. Since 2017, AUTO’s increased its R&D department 3x, from 49 to 149. The company owns 295 patents with another 559 pending. At the current rate, AUTO is granted more than one patent per week for its technology.

It’s hard to overstate the impact of AUTO’s scale advantages against its peers. The more money AUTO invests in its technology, the harder it is for competitors to match its customer value proposition.

This, of course, leads to more customers choosing AUTO for their warehouse fulfillment needs, thus restarting the R&D investment cycle.

AUTO’s Revenue Model: New Customers, Existing Customers, Repeat Revenue

AUTO deploys a land-and-expand business model. The company lands by building the initial cubic storage infrastructure and robot deployment. From there, AUTO has a few levers it can pull.

First, the company can expand with its customer on the initial site via site extensions. Swedish online retailer Boozt.com (BOOZT) is a great example. The company grew from 21 installations in 2017 to 470 by 2021.

The second way AUTO grows revenues is through new site developments. Regional supermarket H.E.B., for example, added two new sites in 2020 and 2021.

Finally, AUTO can generate high-margin revenue through its software subscription service and spare parts business. Think of the spare parts business like TransDigm (TDG), where various AUTO customers can shop for parts from other AUTO customers.

AUTO’s land and expand model works well. 70% of the company’s 2017 customers have returned to place additional orders. This doesn’t include revenue from new customers onboarded since 2017!

Most importantly, 68% of AUTO’s total intake comes from eCommerce orders, which provides a strong tailwind for sustained revenue growth.

We know how the company generates revenue. But let’s get specific.

AUTO’s revenues flow through two segments:

Order book

Order intake

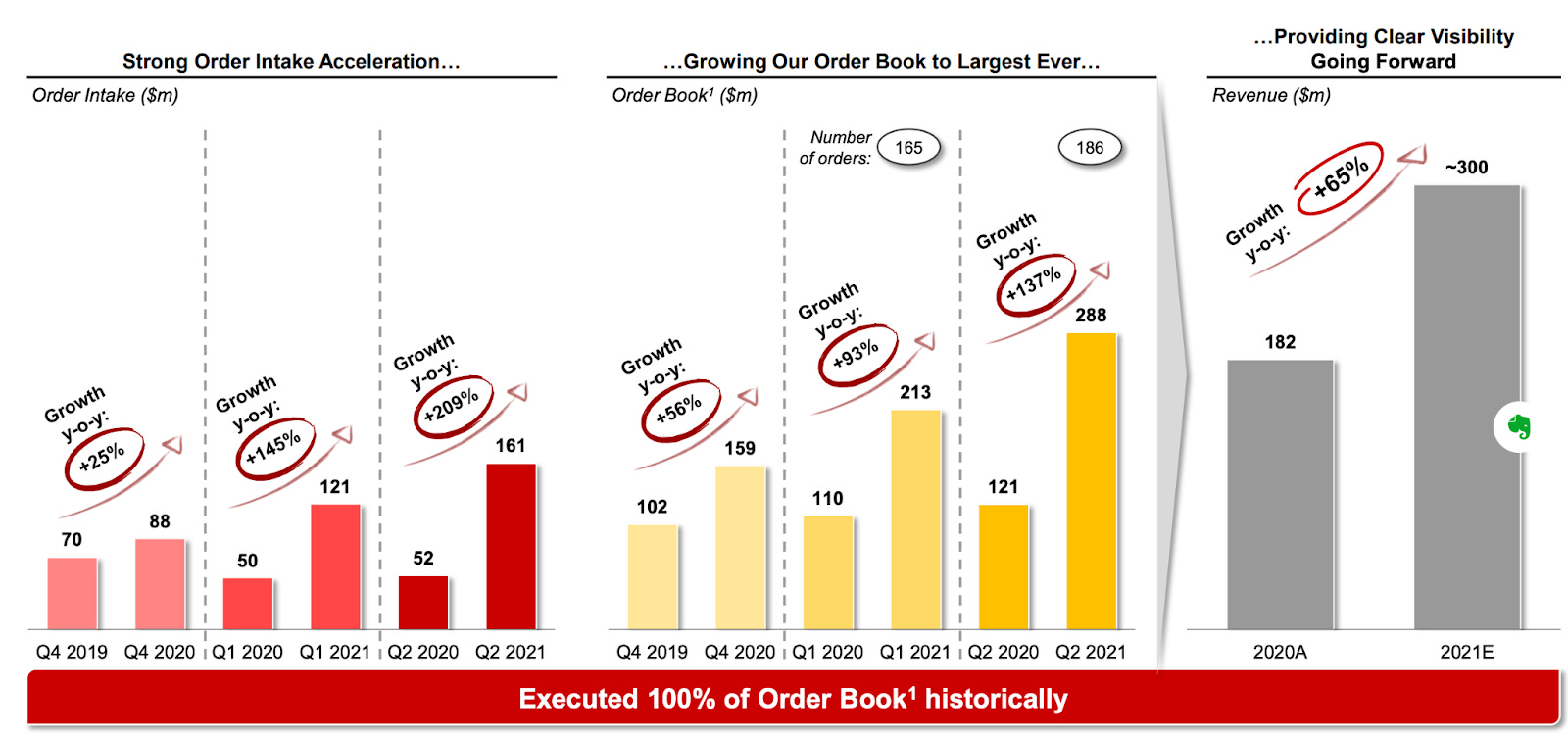

The higher the order book, the more orders are available for AUTO to intake, which translates into higher dollar revenues.

Here’s how it looks below.

Record order books translate to sustained (and record-breaking) revenue growth.

AUTO’s Torrid Revenue Growth Pace

Historically, AUTO's revenues have grown at a ~47% CAGR since 2010. Remarkably, the company’s outdoing its historical growth rates over the last year.

For example, AUTO increased revenue by 69% YoY in Q1 and another 103% YoY in Q2.

More importantly, AUTO’s growth comes without margin compression. The company’s maintained ~50% EBITDA margins and ~84% FCF conversion over the past year.

Yet all that’s in the rearview mirror. What does the future hold?

No Brakes On AUTO’s Growth Train

AUTO has a couple levers to pull for sustained 40-50% top-line revenue growth. First, the company boasts a $3.4B order book. AUTO’s existing customers generated an additional 53% YoY growth in order book backlog.

Collectively, the company has ~2,000 projects from 1,800 customers already in the works.

Then there’s AUTO’s partnership with SoftBank (the investment company bought a 40% stake in AUTO this year). SoftBank’s strategic investment enables the company to penetrate the highly profitable APAC region. AUTO also has access to over 200 of SoftBank’s portfolio companies. 79% of which generate revenues inside the APAC region.

Finally, AUTO is locked in a large lawsuit against Ocado Group (OCADO) for patent infringement.

A win for AUTO would likely result in hundreds of millions of dollars in infringement payments made from OCADO to AUTO over the next few years. Not to mention eliminating one of AUTO’s strongest competitors.

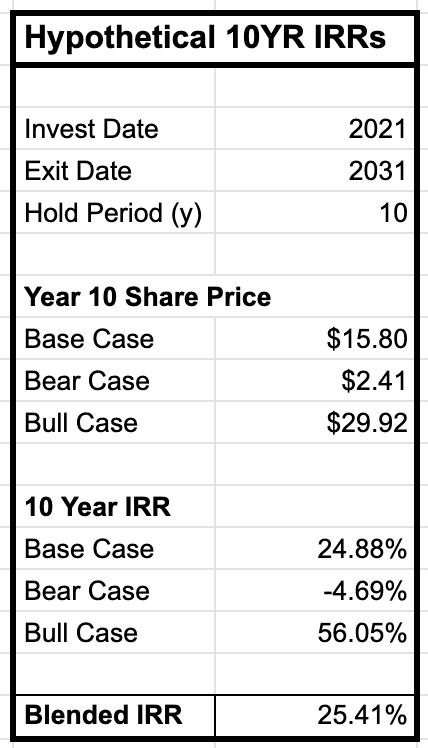

What Could AUTO Look Like In 10 Years?

So what could AUTO look like by the end of the decade?

The management’s target is ~40% organic revenue growth and historical 40-42% EBIT margins. Let’s also assume multiples compress towards some roughly normal range between 3-7x sales and 15-30x EBIT.

The result is a business doing between $8-$10B in revenue, $5-$7B in gross profit, and $3-$4B in EBIT.

Applying our normalized multiples gets us between $15-$38/share in shareholder value or a 25% 10YR IRR on a blended basis.

AUTO is one of the few businesses that occupy the Rule of 100 club is 65% revenue growth + 52% EBITDA margins.

The company has a massive scale advantage against its competition, with over 44x as many warehouse installations.

Over time, AUTO should leverage scale advantages to increase revenue, deepen its patent-protected moat, and capture an even greater share of its $230B end market.

Finally, the company could see a significant positive catalyst should it win the Ocado lawsuit. A win against Ocado would force OCADO to play by AUTO’s rules, giving AUTO a portion of all future Ocado revenues.

But most importantly, it would signal a step-change in the customer value proposition, leaving only AUTO as the most logical choice for an industry set to explode with growth.